Chapter 44 — Money and Banking

Cambridge International AS & A Level Economics (9708) · Unit 9.4 · 4th edition coursebook

Learning objectives

- define the meaning of money

- explain the functions and characteristics of money

- define the meaning of money supply

- analyse the quantity theory of money

- explain the functions of commercial banks, including providing deposit accounts; lending money; holding or providing cash, securities, loans, deposits, equity; reserve ratio and capital ratio; the objectives of commercial banks

- analyse the causes of changes in the money supply in an open economy, including credit creation, government deficit financing, quantitative easing, change in the balance of payments

- explain the role of the bank credit multiplier

- explain the role of the central bank

- evaluate the effectiveness of policies to reduce inflation

- explain demand for money (liquidity preference theory)

- evaluate interest rate determination according to both the loanable funds theory and the Keynesian theory.

Key terms

- money

- an item which is generally acceptable as a means of payment.

- double coincidence of wants

- a situation where two people each have something the other one wants.

- money supply

- the total amount of money in an economy.

- narrow money

- money that can be spent directly.

- broad money

- money used for spending and saving.

- quantity theory of money

- the theory that links inflation in an economy to changes in the money supply.

- Fisher equation

- the statement that MV = PT.

- demand deposit account

- a bank account that allows the holder to make and receive payments.

- savings deposit account

- a bank account which pays interest and may require notice to be given before money can be withdrawn from it.

- government securities

- bills and bonds issued by the government to raise money.

- equities

- shares in firms.

- overdraft

- permission to spend more than is in a demand deposit account.

- loan

- a sum of money lent at an agreed rate of interest for a specific time period.

- reserve ratio

- the proportion of liquid assets to total liabilities.

- capital ratio

- a bank's available financial capital as a percentage of its riskier assets.

- liquidity

- the ability to turn an asset into cash quickly and without loss.

- bank credit multiplier

- the process by which banks can make more loans than deposits available.

- quantitative easing

- a situation where a central bank buys government and private securities from the private sector in order to increase the money supply and so stimulate economic activity.

- total currency flow

- the net amount of money that flows into or out of the country as a result of international transactions.

- economic and monetary union

- co-ordination of policies and the operation of a single currency by a group of countries.

- liquidity preference

- a Keynesian concept that explains why people demand money.

- transactions motive

- the desire to hold money for the day-to-day buying of goods and services.

- precautionary motive

- a reason for holding money for unexpected or unforeseen events.

- active balances

- the amount of money held by households or firms for possible near-future use.

- speculative motive

- a reason for holding money with a view to make future gains from buying financial assets.

- idle balances

- the amount of money held temporarily as the returns from holding financial assets are too low.

- liquidity trap

- a situation where interest rates cannot be reduced any more in order to stimulate an upturn in economy activity.

44.1Introduction to money

Money is an item that people use to buy and sell goods and services, and to perform several other functions. Bank notes and coins (cash) are used mainly for small purchases. Money held in bank deposits is now the main form of money, transferred from one person to another by direct debit, credit cards, debit cards and smartphones.

More recently, cryptocurrencies — sometimes also called digital money or electronic money — have appeared. They allow people to make and receive payments online, person to person, without the need for a commercial bank, and they are not regulated by central banks. Whether cryptocurrencies count as money is debatable, however, because they have not yet become generally acceptable: the majority of shops and firms still do not accept them as a means of paying for products.

The functions of money

Money carries out four classical functions:

- Medium of exchange. Money allows goods and services to be exchanged indirectly, overcoming the need for the double coincidence of wants — the requirement under barter that the two parties to a trade each have what the other one wants.

- Store of value. Money enables people to save. They can hold on to money they receive from selling goods and services for future use.

- Unit of account. Also known as a measure of value, this function allows the value of different items to be compared because prices are expressed in money terms.

- Standard of deferred payment. Money lets people, firms and the government borrow and lend and buy and sell forward — a debt incurred today can be repaid in a known money amount at an agreed future date.

The characteristics of money

To act as money, an item has to possess a number of characteristics:

- Generally acceptable. The most important characteristic. If people will not accept the item in exchange for products, it will not function as money. When confidence in a currency collapses — for instance, during hyperinflation — people switch to a different currency.

- Recognisable. People must be able to identify the item as money. Central banks make the country's notes and coins distinctive.

- Portable. Money has to be easy to carry. Bank notes are light and coins are not too heavy; electronic transfers involve no physical carrying at all.

- Divisible. Money has to come in different denominations so that purchases of different values can be made.

- Homogeneous. Each unit of money has to be identical to every other unit of the same denomination — otherwise people start to hoard the more valuable units.

- Limited in supply. If supply were unlimited, money would have no value and would not be acceptable.

- Not easy to counterfeit. If counterfeiting is easy, the currency loses value. Central banks build security features into notes to prevent counterfeiting.

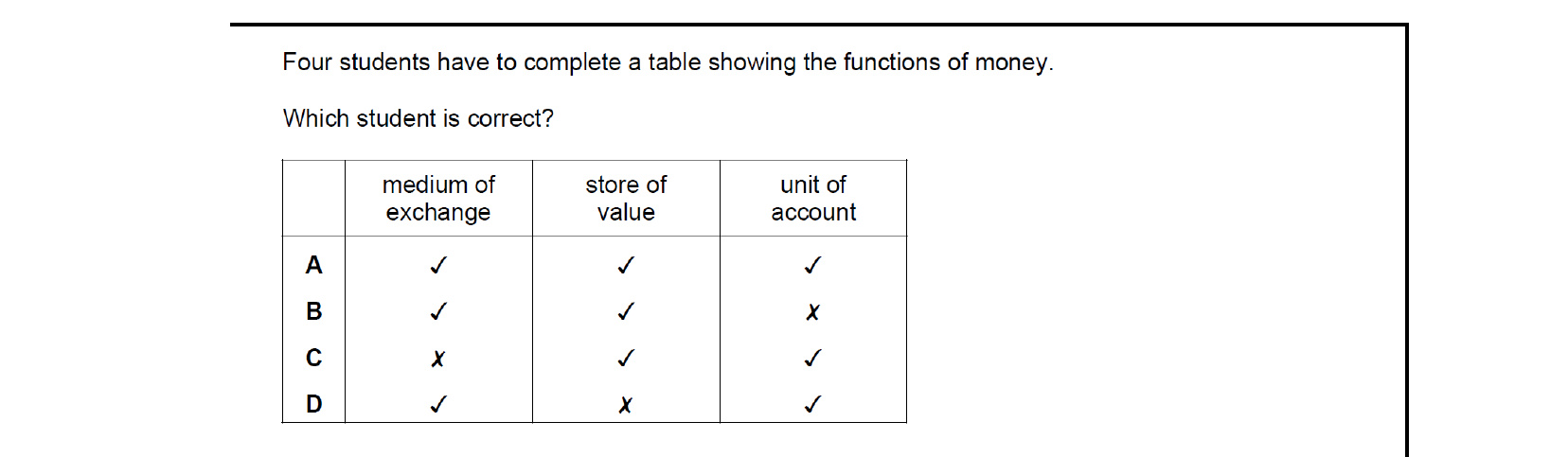

Money has four standard functions: medium of exchange, store of value, unit of account, and a standard of deferred payment. Only option C — 'it is a standard of deferred payment' — names one of these functions; divisibility, portability and acceptability are characteristics money should possess, not functions it performs.

Money simultaneously serves as a medium of exchange (it settles transactions), a store of value (it preserves purchasing power over time) and a unit of account (it provides a common measure of value). The student whose table ticks all three functions — option A — is the only one who has correctly identified what money does.

44.2The money supply

The money supply is the total amount of money in an economy. It consists of currency in circulation plus relevant deposits. Governments measure the money supply to learn about trends in aggregate demand, the state of financial markets and the direction of monetary policy.

In practice, measuring the money supply is not straightforward, because it is hard to decide which items to include. Economists treat items as money if they perform the functions of money — but the extent to which different items perform those functions varies and changes over time. Governments therefore use a variety of measures of the money supply, occasionally altering them to reflect developments in how particular instruments are used.

Two main measures are used:

- Narrow money — money used as a medium of exchange, consisting of notes in circulation and cash held in banks and in balances held by commercial banks at the central bank. This is sometimes called the monetary base.

- Broad money — the items in narrow money plus a range of items that perform the store-of-value function, such as money in savings accounts.

Liquidity is the speed and certainty with which an asset can be turned into cash at its full value without loss. The definition that matches this is option C — the ease with which an asset can be converted into cash. The other options describe foreign-exchange dealing, lender-of-last-resort operations and crisis response, not liquidity.

44.3The quantity theory of money

Aggregate demand is influenced by the money supply and, in turn, can influence the money supply. The quantity theory of money seeks to explain how changes in the money supply affect the economy. It is built on the Fisher equation: MV = PT (also written MV = PY), where M is the money supply, V is the velocity of circulation (the number of times money changes hands), P is the price level, and T (or Y) is the volume of transactions or output.

Because both sides of the equation represent total expenditure in the economy, they always equal each other. To turn the equation into a theory, monetarists add the assumption that V and T are constant — not affected by changes in the money supply — so that a change in M causes an equal percentage change in P. On that view, inflation is fundamentally a monetary phenomenon. Keynesians reject this assumption: they argue that V and T can change when the money supply changes, so no firm prediction can be made about the effect on P from the equation alone.

Key concept link — Equilibrium and disequilibrium

The two sides of the Fisher equation will always move to equilibrium. What is significant is what may cause the equilibrium to change. For example, expectation that the inflation rate will rise is likely to cause the velocity of circulation to increase. People will want to spend the money quickly. They will not want to hold on to money as they will expect its value to fall.

Keynesian and monetarist theoretical approaches

Keynesians follow the work of John Maynard Keynes. They believe that, if left to market forces, the economy may fail to reach a full-employment level of GDP — and that GDP can deviate from full employment by a large amount, for long periods. In such situations they favour government intervention to influence the level of economic activity, including the use of budget deficits to raise aggregate demand when unemployment is high. For most Keynesians, the avoidance of unemployment is the key priority.

Monetarists — most famously associated with Milton Friedman — make the control of inflation the top priority of macroeconomic policy. They argue that inflation is the result of excessive growth in the money supply, so the central role of government is to control the money supply. They also argue that attempts to reduce unemployment by increasing government spending will only raise inflation in the long run, and that the economy is inherently stable unless disturbed by erratic changes in the growth of the money supply.

Monetarists hold that inflation is essentially a monetary phenomenon, so policy makers should follow strict, predictable rules targeting the money supply rather than discretionary fine-tuning (option B). The other statements reflect Keynesian views — instability, sticky wages, gently sloping AS — and are not monetarist.

44.4Functions of commercial banks

Commercial banks (also called high street banks or retail banks) provide a range of services. They offer deposit accounts of two main kinds: a demand deposit account (also called a current account or sight account), which gives easy and quick access to money and is used mainly for receiving and making payments; and a savings deposit account, used mainly as a way of saving and typically paying interest.

Banks hold a range of assets alongside their deposits, including cash, government securities and equities. Most of their profits come from lending. Customers may be allowed to overdraw a demand deposit account by an agreed amount, or to take out an overdraft — useful for unexpected gaps between spending and income, with interest charged on the overdrawn amount. A loan is agreed with the bank for a specific purpose and a specific period, with interest payable on the full value of the loan whether it is used or not; the interest rate on a loan is normally lower than on an overdraft.

The proportion of liquid assets to total deposits a bank keeps is the reserve ratio. The bank's available financial capital as a percentage of its riskier assets is the capital ratio.

The objectives of a commercial bank

Commercial banks pursue three main objectives: profitability, liquidity and security. They aim to generate high profits for shareholders, mainly by lending. This objective conflicts with the other two, so a balance has to be struck. They must hold enough liquid assets — cash and short-term securities that can be turned into cash quickly — to meet expected customer demands for withdrawals; these liquid assets, however, are not very profitable (cash earns nothing at all). They must also have enough financial capital to cover their riskier loans, to convince customers that they are financially sound and to absorb losses. A bank will therefore keep some assets that are liquid but not very profitable and some that are profitable but not very liquid, and may retain some profits to cover the possibility that borrowers default or that firms in which the bank holds shares go out of business.

Key concept link — The margin and decision making

As economic activity changes, commercial banks have to review the balance of their objectives.

44.5Causes of changes in the money supply

There are five main causes of an increase in the money supply in an open economy:

- an increase in commercial bank lending

- an increase in government spending financed by borrowing from commercial banks

- an increase in government spending financed by borrowing from the central bank

- the sale of government bonds to private sector financial institutions (quantitative easing)

- more money entering than leaving the country.

Commercial banks and credit creation

When a commercial bank makes a loan it creates money. The borrower's account is credited with the amount borrowed, and that new deposit is itself money. Banks are in a powerful position to do this because they can create more deposits than they hold in cash and other liquid assets. From experience, banks know that only a small proportion of deposits are ever actually cashed — most payments are made through credit cards, debit cards or online transfers, which simply move balances between accounts rather than physically withdrawing cash. So banks can create deposits in excess of their liquid assets.

They still have to manage their liquidity ratios with care — the lower the proportion of liquid assets they keep, the more they can lend, but the bigger the risk that they cannot meet their customers' demands for cash. If they keep too low a ratio, or if depositors suddenly start to cash more of their balances, the bank may face a run. Banking is based on confidence: customers have to believe there is enough cash to pay them out, even though, in practice, there is not — at least not all at once.

The bank credit multiplier

Using its reserve ratio, a bank can calculate its bank credit multiplier:

Bank credit multiplier (after loans have been made) = Value of new assets created / Value of change in liquid assets.

So if total deposits rise by $600 million as a result of a new cash deposit of $100 million, the multiplier is $600m / $100m = 6. The multiplier can also be calculated in advance:

Bank credit multiplier (in advance) = 100 / liquidity ratio.

Reserve ratio

If a bank keeps a reserve ratio of 5%, the bank credit multiplier is 100 / 5 = 20. With this knowledge the bank can work out how much it can lend. The potential increase in total liabilities is the change in liquid assets multiplied by the bank credit multiplier; if liquid assets rise by $40 million and the multiplier is 20, total deposits can rise by $40m × 20 = $800m. The change in loans is then the change in liabilities minus the change in liquid assets — because part of the rise in liabilities goes to the people putting in the new liquid assets. In this example loans rise by $800m − $40m = $760m.

In practice a bank may not lend the full amount the multiplier implies. There may be too few households and firms wanting to borrow, or too few credit-worthy borrowers. Lending heavily to borrowers with poor credit ratings carries a high risk of default that can in turn threaten the bank's liquidity. A bank will change its reserve ratio if depositors alter the proportion of their balances they want in cash, if other banks change their lending policies, or if the central bank requires the bank to hold a different ratio. A central bank may also influence commercial banks' ability to lend through open market operations — buying or selling government securities. To reduce bank lending, it sells government securities; the purchasers pay by drawing on their deposits in commercial banks, which reduces commercial banks' liquid assets and so their capacity to lend.

The capital ratio

The capital ratio is a commercial bank's available financial capital expressed as a percentage of its riskier assets. Available financial capital includes retained profits and newly issued shares. Government securities are normally treated as carrying no risk, but some loans count as risky. A capital ratio of 8% means that 8% of the bank's riskier assets are covered by readily available financial capital. The higher the ratio, the more unexpected losses the bank can absorb without going out of business. The capital ratio is designed to protect customers in a financial crisis and to promote the stability of the banking sector by discouraging excessive risk taking.

The role of a central bank

A central bank issues bank notes and authorises the minting of coins. It is the bank of the commercial banks — commercial banks keep deposits at the central bank, which lets them make and receive payments to and from other commercial banks and withdraw money when needed; these deposits count as liquid assets. The central bank also usually lends to commercial banks that get into financial difficulty, acting as a lender of last resort. Two of its other key functions are to act as banker to the government and to implement the government's monetary policy.

Government deficit financing

If the government spends more than it raises in taxation, it has to borrow. This is organised by the central bank. If the central bank borrows on the government's behalf by selling government securities to the non-bank private sector (non-bank firms and the general public), it uses existing money: the purchasers draw on their bank deposits to buy the securities, so the rise in liquid assets caused by the extra government spending is matched by an equal fall in liquid assets as the public withdraws money to buy the securities. The money supply does not change.

If, however, the deficit is financed by borrowing from commercial banks or from the central bank itself, the money supply does increase. When the government borrows from the central bank, it spends money drawn from its account at the central bank; this spending raises deposits in commercial banks and so raises their liquid assets, allowing them to lend more. If the government borrows from commercial banks by selling them short-term government securities, those securities count as liquid assets and so can also be used as the basis for further lending.

Quantitative easing

When the rate of interest is already very low, a central bank may try to raise aggregate demand through quantitative easing. This involves the central bank buying both government and private securities of different maturities from financial institutions, including commercial banks. In return for the securities, the central bank credits the accounts of the commercial banks; with more liquid assets, the commercial banks are expected to lend more. This should raise the money supply and reduce short-term and long-term interest rates, which in turn should boost investment, consumer expenditure and so aggregate demand and economic activity. Quantitative easing has also been used to support specific markets that are in difficulties, such as the purchase of mortgage-based securities to support a housing market.

Changes in the balance of payments

The total currency flow is the net inflow or outflow of money resulting from all international transactions recorded in the balance of payments. If, for example, export revenue exceeds import expenditure, money flows into the country on the trade balance. Exporters deposit the inflows in the country's commercial banks, raising their liquid assets and so producing a multiple increase in the money supply.

44.6The effectiveness of policies to reduce inflation

Contractionary monetary or fiscal policy can be used to reduce inflation. Supply-side policy can also be useful where inflation is of the cost-push type — for example, increased spending on training can raise labour productivity and so reduce labour costs, or at least the upward pressure on them. Lower corporate tax may encourage firms to buy more efficient capital equipment, which can also restrain price rises.

How effective these policies are depends on a number of factors. One is whether the type of inflation has been correctly identified. If inflation is cost-push, but the government responds with contractionary fiscal and monetary policy, the fall in aggregate demand may leave the price level largely unchanged while raising unemployment. In practice, distinguishing cost-push from demand-pull inflation is hard — once inflation is under way it is usually a mix of the two — and some policy tools help to deal with both types in the long run. Higher spending on education and training, for example, may add to demand-pull inflation in the short run but reduce cost-push inflation in the long run by raising productivity.

Governments and central banks make forecasts of future inflation, and the further into the future those forecasts reach, the less reliable they become. By the time a policy has been chosen, implemented, and households and firms have reacted, the inflation problem may have faded — and the policy may then simply deepen any downturn.

There may be limits on the tools a government can use. Membership of an economic and monetary union rules out setting the country's own interest rate. Any country may be reluctant to raise income tax for fear of pushing skilled workers to emigrate or discouraging multinationals from setting up. A government may want to spend more on infrastructure to reduce cost-push inflation but be unable to do so because tax rises are unpopular and willing lenders are scarce.

A government may also decide that inflation is the result of the money supply growing faster than output, but controlling the money supply is hard. Commercial banks have a profit incentive to lend more, and are inventive in getting around any limits on bank lending.

One of the main influences on the effectiveness of anti-inflationary policy is how households and firms react. Contractionary policies are typically introduced when optimism is high — and in those conditions, a higher rate of interest may not reduce consumption and investment much. A higher rate of income tax may simply prompt people to work longer hours to defend their living standards rather than spend less. Training subsidies to firms may not raise productivity if firms do not also have the capital equipment to make use of the new skills. If wages rise by more than productivity, production costs continue to rise.

Key concept link — The role of government and the issues of equality and equity

Anti-inflationary policy tools have a different impact on different income groups. For example, a cut in government spending on healthcare is likely to have more of a negative effect on the poor than on the rich.

The monetary transmission mechanism

The monetary transmission mechanism is the process by which a change in monetary policy works through the economy — via a change in aggregate demand — to the price level and real GDP. The chain runs from the policy change (for example, an increase in the money supply) to a fall in the interest rate, to a rise in aggregate demand, to higher output and/or a higher price level.

44.7The liquidity preference theory

The demand for money is explained by liquidity preference. There are three main motives for households and firms to hold part of their wealth as money.

The first is the transactions motive — the desire to hold money to make everyday purchases and meet everyday payments. The amount held depends on the income received and the frequency of payments: the higher the income and the less frequent the receipts, the larger the balance held.

The second is the precautionary motive — households and firms typically hold rather more money than they expect to spend, so as to meet unexpected expenses and take advantage of unforeseen bargains. Balances held for the transactions and precautionary motives are sometimes called active balances, since they are likely to be spent in the near future. They are relatively interest-inelastic: a rise in the interest rate does not cause households and firms to cut these balances significantly.

The third motive, the speculative motive, is interest-elastic. Households and firms hold idle balances when they believe the returns from holding financial assets are low. One important financial asset is government bonds, which represent loans to the government. The price of a bond and its effective interest rate move in opposite directions: a bond with a face value of $500 carrying a fixed interest rate of 5% pays an income of $25 each year regardless of the bond's market price, so if the price rises to $1000 the effective yield falls to 2.5%. Households and firms are therefore likely to hold money rather than bonds when bond prices are high and expected to fall — they sacrifice little interest income, and they avoid the capital loss that would follow a fall in bond prices. Speculative demand for money is low when bond prices are low and the rate of interest is high.

The total demand for money — the sum of transactions, precautionary and speculative balances — gives the downward-sloping liquidity preference curve (see Figure 44.9). The curve is relatively steep at high interest rates (active balances dominate) and flattens at low rates (the speculative motive becomes the more elastic component).

44.8Interest rate determination

Keynesians argue that the rate of interest is determined by the demand for and supply of money. They assume that the supply of money is set by the monetary authorities and is fixed in the short run.

On a diagram with the rate of interest on the vertical axis and the quantity of money on the horizontal axis, the liquidity preference curve (the sum of the transactions, precautionary and speculative demands for money) slopes down from left to right, and the money supply curve is a vertical line. They cross at the equilibrium rate of interest. An increase in the money supply shifts the vertical money supply line to the right, lowering the rate of interest: households and firms find themselves holding more money than they want, use the excess to buy financial assets, the price of government bonds rises and the effective interest rate falls (see Figure 44.10).

The liquidity trap

Keynes described one situation in which an increase in the money supply does not pull the interest rate down — the liquidity trap. It occurs when the rate of interest is already very low and bond prices are correspondingly very high. Speculators expect bond prices to fall in the future, so any extra money supplied by the central bank is simply held — speculators will not buy bonds for fear of a capital loss and because the yield is so low anyway. On the diagram (see Figure 44.11), the liquidity preference curve becomes perfectly elastic at this rate, and a rightward shift of the money supply line leaves the interest rate unchanged.

Loanable funds theory

An alternative view is that the rate of interest is determined by the demand for and supply of loanable funds (see Figure 44.12). The demand for loanable funds is the demand to borrow — households borrow to buy cars and houses, firms borrow because they are in financial difficulty or, more commonly, because they want to invest, and the government borrows when it runs a budget deficit. The demand curve slopes down from left to right because the lower the rate of interest, the more economic agents will want to borrow.

The supply of loanable funds comes from savings: the more money is saved, the more is available to lend. The supply curve slopes up from left to right because the higher the rate of interest, the greater the return to saving and the more economic agents will save. An increase in saving shifts the supply curve to the right and brings the rate of interest down to a new, lower equilibrium (see Figure 44.13).

End-of-chapter practice

Past-paper questions from CIE 9708. Pick A, B, C or D. Answers are saved on this device — press Download report (PDF) at the top to save them.

Bonds pay a fixed coupon, so when their market price rises the yield (effective interest rate) falls, and vice versa. This inverse relationship between bond prices and interest rates is central to Keynes's speculative motive: investors hold money when they expect bond prices to fall (interest rates to rise). The correct statement is option D.

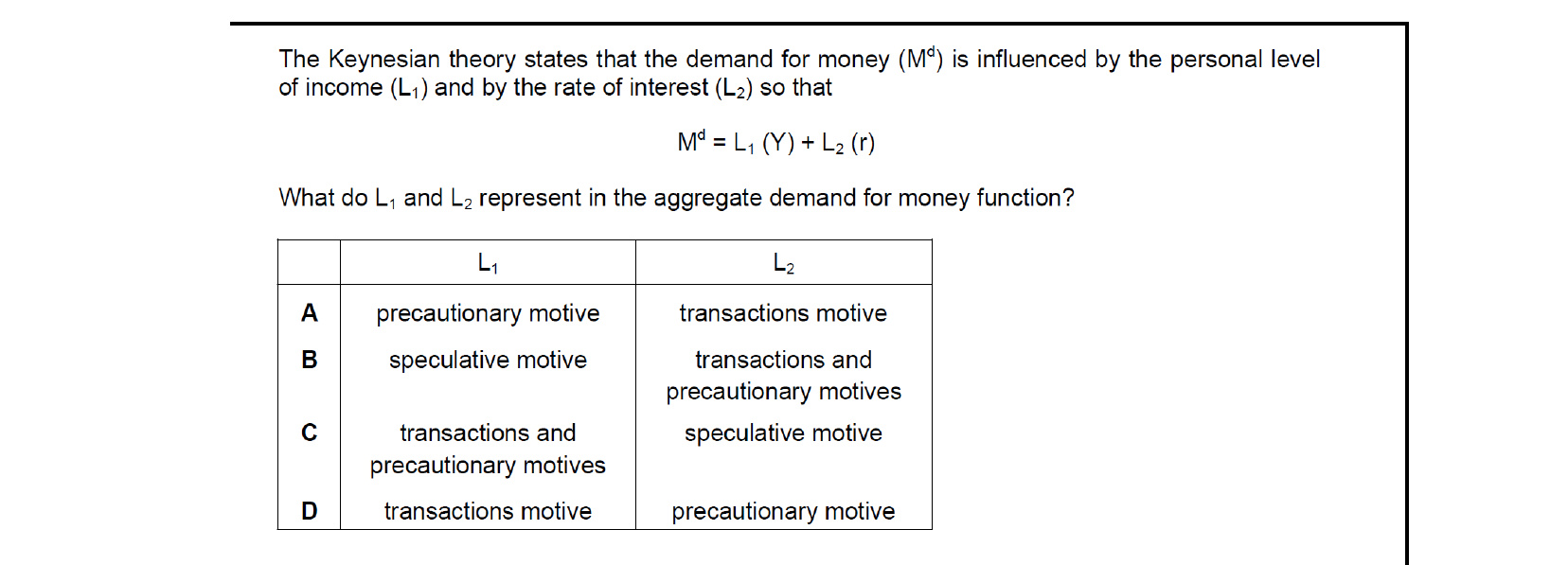

In the Keynesian demand-for-money function L1(Y) depends on income and L2(i) depends on the interest rate. The income-dependent component captures the transactions and precautionary motives (money held for spending and contingencies), while the interest-dependent component captures the speculative motive — exactly the pairing in option C.

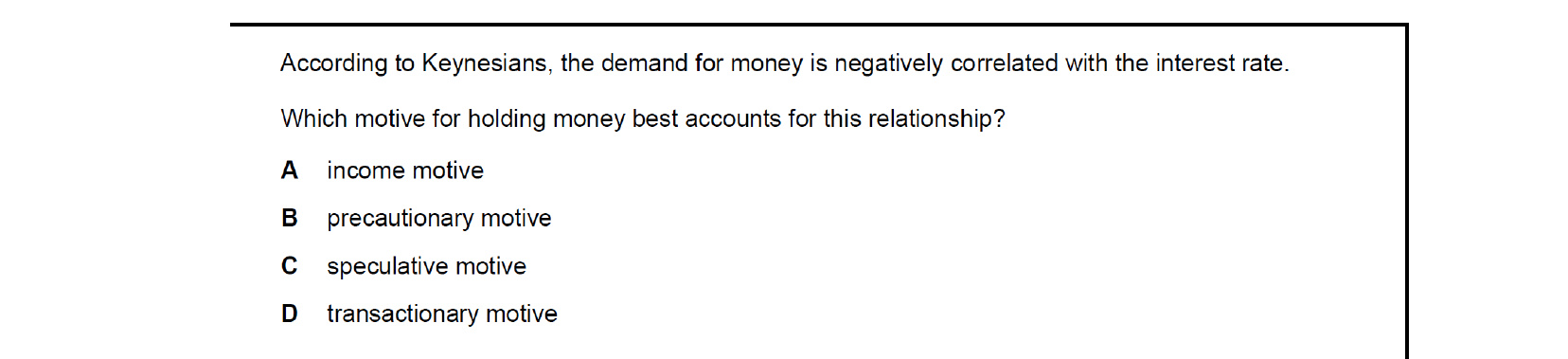

The transactions and precautionary motives depend mainly on income, not on the interest rate. Only the speculative motive (option C) generates a negative relationship between the demand for money and the interest rate: when rates are low, bond prices are high and likely to fall, so people hold more money rather than risk a capital loss.

If a net outflow of currency on trade/capital account turns into a net inflow (option A), more foreign currency is sold to the banking system in exchange for domestic currency, raising the reserves of commercial banks and increasing the money supply via the bank credit multiplier. The other options would tighten the money supply.

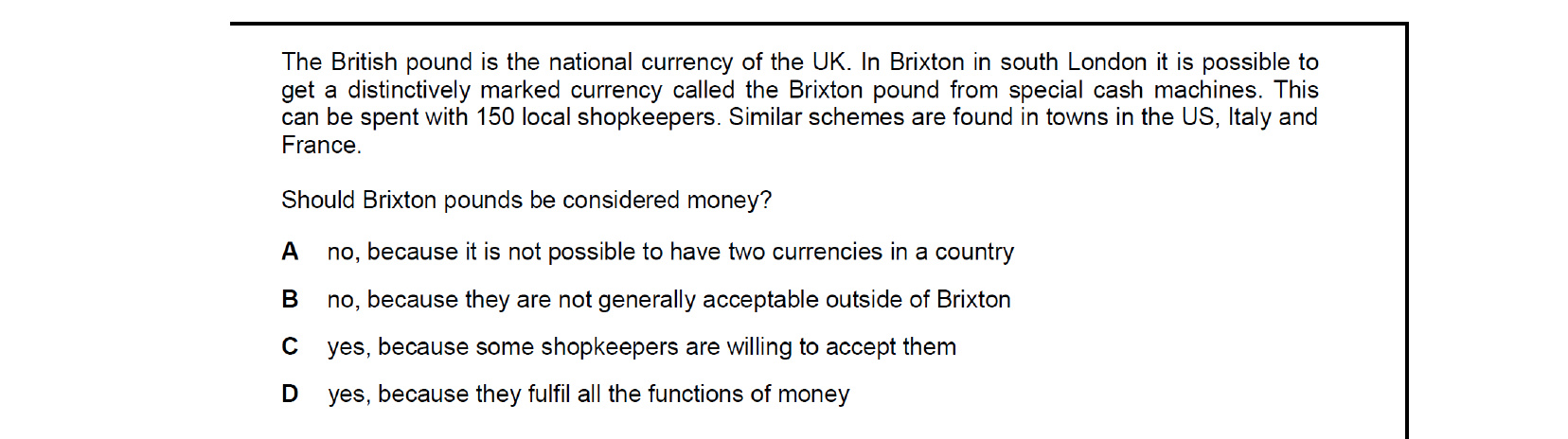

Whether something counts as money depends on whether it performs money's functions for a defined group of users. Inside Brixton, the Brixton pound serves as a medium of exchange, store of value, unit of account and standard of deferred payment among the 150 participating shopkeepers and their customers, so it does count as money — option D.

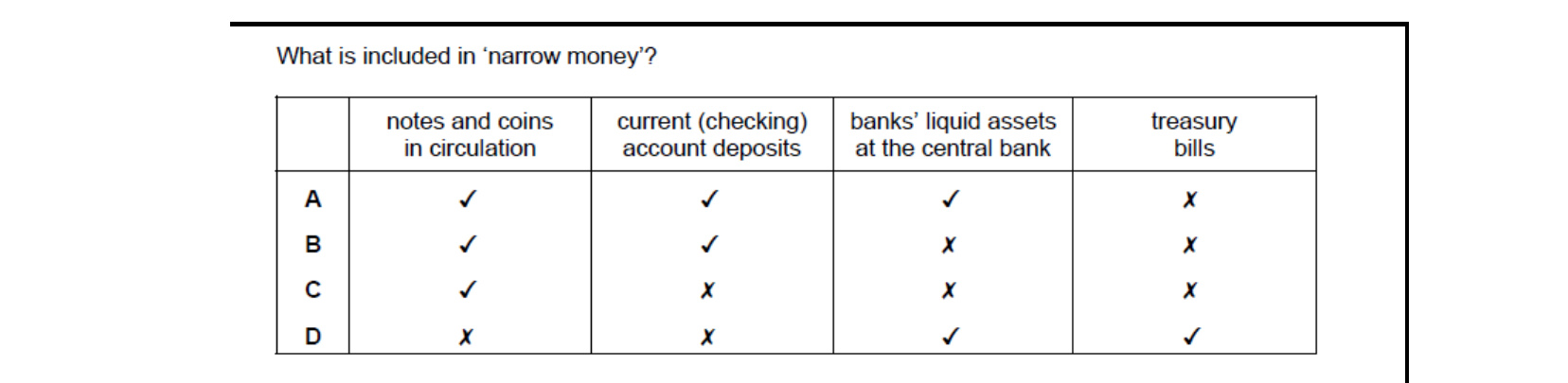

Narrow money (M1) is the most liquid component of the money supply — typically notes and coins in circulation plus instantly-available current (sight) account deposits. It excludes longer-dated assets such as Treasury bills, which are part of broader monetary aggregates. The row matching this composition is option A.

Attempt the practice questions above to build your score.

Self-evaluation checklist

After studying this chapter, you should be able to:

- Understand that money acts as a medium of exchange, store of value, unit of account and standard of deferred payments

- Explain the functions and characteristics of money: acceptable, recognisable, portable, divisible, homogeneous, limited in supply and not easy to counterfeit

- Understand that money supply includes notes, coins and money in bank accounts

- Analyse the quantity theory of money which proposes that an increase in the money supply will cause an equal percentage change in the price level

- Explain the functions and the key objectives of commercial banks (profitability, liquidity and security)

- Analyse the four main causes of changes in the money supply in an open economy: credit creation, government deficit financing, quantitative easing, change in the balance of payments

- Explain that the bank credit multiplier shows how much money a commercial bank can create by lending

- Describe the role of the central bank

- Evaluate the effectiveness of anti-inflationary policies

- Understand that the demand for money is explained by the liquidity preferences of households and firms

- Consider the Keynesian view of interest rate determination that the rate of interest is determined by the demand for and supply of money, compared with the loanable funds theory that suggests that the rate of interest is determined by the demand for and supply of loanable funds

Want more practice? Drill this chapter's past-paper MCQs (135 questions) →