Chapter 15 — National Income Statistics

Cambridge International AS & A Level Economics (9708) · Unit 4.1 · 4th edition coursebook

Learning objectives

- Define the meaning of national income.

- Explain the purpose of national income statistics.

- Explain the difference between gross domestic product (GDP), gross national income (GNI) and net national income (NNI).

- Analyse the three methods of measuring GDP.

- Explain how measures of national income are adjusted from market prices to basic prices.

- Explain how measures of national income are adjusted from gross values to net values.

Key terms

- national income

- A country's total output.

- national income statistics

- Measures of the total output (income and expenditure) of an economy.

- gross domestic product (GDP)

- The total output produced in a country.

- gross national income (GNI)

- GDP plus net income from abroad.

- net property income from abroad

- Receipts of profit, rent and interest earned on the ownership of foreign assets minus the payments of profit, rent and interest to non-residents.

- compensation of employees

- Income of workers who work in another country for a short period of time.

- gross national disposable income

- GNI plus net transfers of workers' income to their relatives to and from other countries.

- multinational companies (MNCs)

- Firms that operate in more than one country.

- output method

- Measuring GDP by adding up the value of output produced by all firms in an economy.

- income method

- Measuring GDP by adding up the incomes earned by factors of production in an economy.

- expenditure method

- Measuring GDP by adding up the spending on the goods and services produced in an economy.

- market prices

- Prices paid by consumers, inclusive of indirect taxes and after subsidies.

- basic prices

- Prices received by producers, excluding indirect taxes and including subsidies.

- depreciation

- The fall in the value of capital goods over time due to wear and tear.

- net national income (NNI)

- GNI minus depreciation.

15.1National income statistics

National income is the total output produced by a country. The same flow of activity can be looked at three ways: people earn an income from producing the output, and they spend that income on the output, so total output, total income and total expenditure are equal at the national level.

National income statistics is the general term for the family of measures that capture this flow. Governments collect them to assess how an economy is performing — an economy is usually considered to be doing well if its output is growing at a sustained and sustainable rate. International organisations such as the United Nations also use national income statistics to compare countries.

Higher output has the potential to raise living standards. If an economy is growing more slowly than its capacity would suggest, governments are likely to introduce policy to stimulate it. Economists examine both the level of output and the rate of change of output. A larger economy can show a smaller percentage growth rate than a smaller economy in the same year while still adding more in absolute terms, because percentages are calculated from different bases.

Key concept link — time

National income is measured each year and compared both in the short run and long run. For example, a country's national income could be compared with last year's national income and with the national income of fifty years ago.

National income measures factor incomes earned from producing output. Welfare benefit payments are transfer payments — money redistributed by government without any productive activity in return — so they are excluded to avoid double counting. Dividends, overtime pay and rents from government houses are all genuine factor rewards for capital, labour and land respectively, so they are included.

15.2Gross domestic product and gross national income

Gross domestic product

The most widely used measure of national income is gross domestic product (GDP). GDP is used by economists, governments and international organisations to assess what is produced, earned and spent in an economy. 'Gross' means total, 'domestic' means within the home economy, and 'product' means output. A country's GDP is therefore the total value of output produced by factors of production based in that country during a given period (typically a year).

Gross national income

Gross national income (GNI) is an increasingly important measure — the United Nations uses it in its Human Development Index, for example. GNI shifts the focus from output produced inside a country to income earned by the country's residents and firms regardless of where it is earned. To get from GDP to GNI, add net property income from abroad, net receipts of compensation of employees, and net taxes less subsidies on products.

Governments also publish gross national disposable income, which adds the net flow of remittance income — money sent home by people working abroad, minus money sent home by foreign workers based in the country.

Differences in countries' GDP and GNI

For most countries, GDP and GNI are similar. For some, the two measures diverge noticeably. A country with substantial inward investment by foreign multinational companies (MNCs) may have a GDP that exceeds its GNI: foreign firms produce inside the country (raising GDP) but profits flow back out to non-resident owners (so GNI is lower). The opposite case — GNI higher than GDP — arises in countries whose own MNCs invest heavily abroad and repatriate profits, or whose citizens work abroad and send income home.

Net national income

Net national income (NNI) takes GNI and subtracts depreciation — the loss in the value of the country's stock of capital goods over the period. NNI is therefore a measure of how much is left for consumption and net investment after replacing the capital used up in production.

GDP measures output produced inside a country's borders; GNI adjusts this for income flows across borders. The only difference is net property income from abroad — interest, profits and dividends earned by residents abroad minus those earned by foreigners domestically. Capital consumption affects the gross-to-net distinction, not GDP-to-GNI.

15.3Methods of measuring GDP

Because total output, total income and total expenditure are different sides of the same flow, GDP can be measured three different ways: the output method, the income method and the expenditure method. Each method should give the same total because they all measure the same circular flow: the value of what is produced equals the income earned producing it (wages, rent, profit and interest), and if all income is spent, expenditure equals that income. In practice the three methods produce slightly different numbers because of data limitations, and statistical agencies typically publish a 'GDP at market prices' figure that reconciles them. The circular flow of income is the underlying logic behind all three approaches.

The output method

The output method — also called the production method — measures the value of output produced by all the industries in the economy. This includes manufacturing, construction, distributive trades, hotel and catering, agriculture, and the wider services sector. To avoid double counting, output must be measured carefully. If the cars sold by a car manufacturer were added to the value of the tyres produced by a separate tyre firm, the tyres would be counted twice — once when sold to the car maker and again as part of the car's price. Two equivalent ways of avoiding this:

- Total only the value of final goods and services — the output sold to its end user.

- Sum the value added at each stage of production. Value added is the difference between what a firm pays for the inputs it buys and the price at which it sells its finished product. For example, if a TV firm buys components and uses them to produce televisions that it sells for a higher price, only the additional value the firm has created at this stage is added to GDP — the value of the components has already been counted at the earlier stage.

Both methods should give the same figure: the market value of the finished output produced in the economy.

The income method

The income method measures GDP by adding up all the incomes earned in producing that output. These incomes are the payments made to the factors of production: wages to labour, rent to land, interest to capital and profit to entrepreneurship. Workers receive wages and entrepreneurs receive profits in return for supplying their factor services. Only payments received in return for providing a good or service count. Transfer payments — movements of income from taxpayers to households (such as state pensions, unemployment benefits or other welfare payments) and from government to firms (such as subsidies) — are excluded, because they do not represent newly created output. They simply redistribute income already earned elsewhere in the economy.

The expenditure method

The expenditure method adds up the spending on the goods and services the economy produces. The standard formulation is C + I + G + (X − M), where:

- C = consumer expenditure (spending by households on goods and services);

- I = total investment, including any changes in stocks (output produced but not yet sold is treated as an addition to stocks and counted as investment, so that the measure still captures everything produced in the year);

- G = government spending on goods and services (welfare and other transfer payments are excluded for the same reason as in the income method — they shift income rather than buy new output);

- (X − M) = net exports. Exports are added because the sale of exported goods represents output produced in the country and generates income for residents; imports are deducted because spending on imports is spending on output produced in foreign countries, generating income for people abroad rather than at home.

A useful way to remember the three methods is to picture the circular flow: production creates output, output creates income, income is then spent — so totalling output, income or expenditure must yield the same figure.

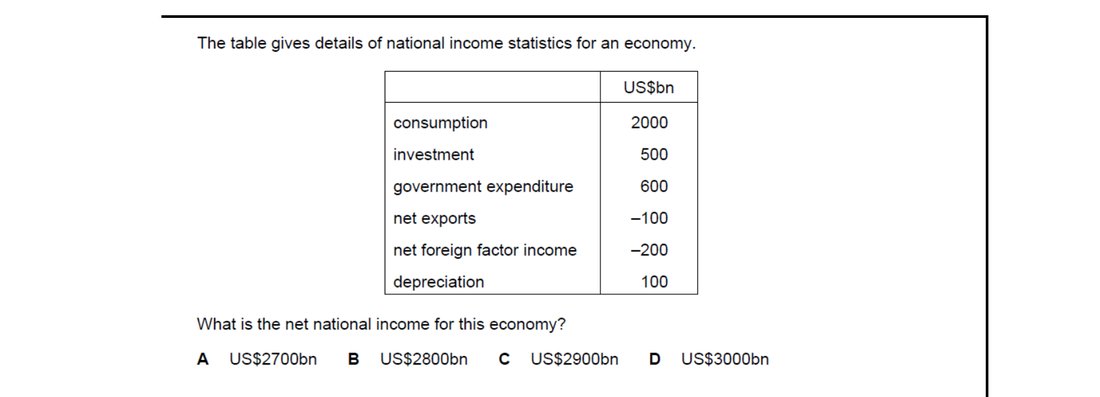

Net national income converts GDP into a national, net measure: add net foreign factor income (to move from 'domestic' to 'national') and subtract depreciation (to move from 'gross' to 'net'). Applying these adjustments to the table entries gives the answer US$2700bn. National debt is a stock of borrowing rather than a flow of current income, so it is ignored.

15.4Market prices and basic prices

The value of output can be measured at two different price points. Market prices are the prices consumers actually pay — they include any indirect taxes (VAT, excise duties) and are net of any subsidies on the product. Basic prices are the prices producers actually receive — they exclude indirect taxes and include subsidies the producer has received.

The two perspectives matter because a tax-and-subsidy regime can drive a wedge between what the consumer pays and what the producer keeps. To convert GDP at market prices to GDP at basic prices, deduct net indirect taxes (indirect taxes minus subsidies). The basic-price measure is closer to a measure of underlying productive activity, while the market-price measure reflects the value of what consumers actually spend.

Market prices include indirect taxes (which add to the price paid) and subsidies (which reduce it). To convert from factor cost — what producers receive — to market prices — what consumers pay — add taxes and subtract subsidies. Option B states exactly this adjustment.

15.5Gross values and net values

The figures for GDP and GNI both include gross investment - the total spending on capital goods over the period. Gross investment is made up of two components. The first is the output of capital goods used to replace existing capital goods that have worn out or become out of date because of advances in technology. The second is the output of capital goods required to expand productive capacity. Adding these together gives gross investment, which is the figure that enters GDP and GNI under the expenditure measure.

Gross investment tells us how much is being spent in total on capital goods. It does not, on its own, reveal whether the country's productive capacity is growing, standing still or shrinking, because some of that spending is simply replacing capital that has been used up.

To answer that question, economists use the net measures. Net domestic product (NDP) is GDP minus depreciation, and net national income (NNI) is GNI minus depreciation. They include only net investment - additions to the capital stock - by deducting the value of the replacement capital goods.

The deducted figure is known as depreciation, also called capital consumption. It measures the value of capital goods that have worn out or become out-of-date over the period.

Net investment matters because it indicates whether the country's ability to produce goods and services in future will increase, stay the same or even decrease:

- If net investment is positive, the capital stock is growing and productive capacity is expanding;

- If net investment is zero, the capital stock is just being maintained;

- If net investment is negative, the capital stock is shrinking and future productive capacity will fall.

Net measures are therefore conceptually closer to a true picture of what the economy has produced for future use. In practice, however, NDP and NNI are less reliable than GDP and GNI because depreciation is hard to estimate consistently - it depends on assumptions about how long capital goods last and how quickly they lose value.

Putting the adjustments together gives a chain that links the different headline measures. Starting from NNI at basic prices, depreciation is added back to reach GNI at basic prices; net property income from abroad is subtracted to reach GDP at basic prices; and indirect taxes are added and subsidies are subtracted to reach GDP at market prices. Working in the opposite direction undoes each step. The same building blocks - depreciation, net property income from abroad, indirect taxes and subsidies - link any pair of these national income measures.

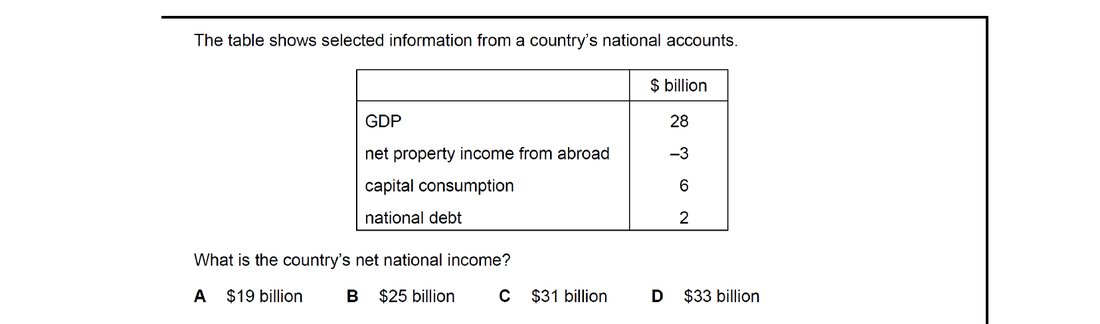

Net national income starts from GDP, then adjusts for cross-border factor incomes and for capital consumption (depreciation of the capital stock used up in production). National debt is a stock of past borrowing rather than a flow of current income, so it is excluded. Applying the gross-to-net and domestic-to-national adjustments to the table figures yields $19 billion.

End-of-chapter practice

Past-paper questions from CIE 9708. Pick A, B, C or D. Answers are saved on this device - press Download report (PDF) at the top to save them.

Only paid economic activity counts in national income. The director loses $80,000 of salary, but earns $60,000 in consultancy fees and $10,000 in dividends (a return on productive capital), while dismissing the gardener removes $8,000 of paid employment income from the economy. Net change: −80 000 + 60 000 + 10 000 − 8 000 = −$18 000.

The income method sums factor rewards — wages, rent, interest and profit — paid for current production. Transfer payments such as pensions and benefits are redistributions of existing income with no corresponding output, so they are excluded to avoid double counting. Income from abroad, profits and rent are all genuine factor incomes and are included.

Real GDP measures output produced within a country's borders. Age-related pensions are transfer payments — government simply redistributes income, with no good or service produced in return — so they are excluded. Dividends from foreign investment, rental income earned by housing authorities and distributed profits all correspond to productive activity and so are included.

Real GDP records factor incomes earned from producing output. Pensions paid to retired people are transfer payments — money redistributed without any current production in exchange — so they are not counted. Profits, rent and wages are all factor incomes paid for current productive activity and so are included in GDP.

Only payments that reward current production count as national income. Unemployment benefits are transfer payments — government redistributes money without any good or service being produced in exchange — so they are excluded. Dividends, retained profits and rent paid to landlords are all factor incomes earned from producing output, and so are all included.

Attempt the practice questions above to build your score.

Self-evaluation checklist

After studying this chapter, you should be able to:

- Define national income and explain why national income statistics matter.

- Distinguish GDP, GNI, and NNI and explain why they differ.

- Describe the three methods of measuring GDP and explain why they should — in principle — give the same answer.

- Convert between market prices and basic prices using net indirect taxes.

- Convert between gross and net values using depreciation.

Want more practice? Drill this chapter's past-paper MCQs (40 questions) →