Chapter 2 — Economic Methodology

Cambridge International AS & A Level Economics (9708) · Unit 1.2 · 4th edition coursebook

Learning objectives

- Explain why economics is a social science.

- Differentiate between facts and opinions (positive and normative statements).

- Explain why economists use the term ceteris paribus.

- Explain when to refer to a time period such as 'short run', 'long run' and 'very long run'.

Key terms

- macroeconomics

- The study of an economy or a group of economies.

- microeconomics

- The study of individual markets (households and firms).

- model

- A simplified view of reality used to explain economic problems and issues.

- positive statement

- A statement that is based on facts or actual evidence.

- normative statement

- A statement that is based on the economist's opinion or value judgement and which cannot be proven.

- ceteris paribus

- A Latin phrase meaning 'other things equal' or 'other things are unchanged'; used by economists to model the effects of one change at a time.

- short run

- Time period when a firm can change at least one but not all factor inputs.

- long run

- Time period when all factors of production are variable but with a constant, such as the state of technology.

- very long run

- Time period when all key inputs into production are variable.

2.1What is economics?

Economics builds on the fundamental economic problem covered in Chapter 1. A simple working definition is that economics is the study of how scarce resources are allocated. The discipline traditionally divides into two branches.

Microeconomics looks at individual markets. It examines how households (consumers) and firms (businesses) behave, the decisions they make, and how they interact with each other. A typical microeconomic question is what factors explain why consumers choose to buy some goods and not others.

Macroeconomics looks at the economy as a whole, or at a group of economies. It also examines how consumers and firms interact, but at a much broader level, and it usually involves the role of government. A typical macroeconomic question is why one economy grows at a faster rate than another.

In practice the boundary between microeconomics and macroeconomics (illustrated in Figure 2.2) is no longer as clear-cut as it once was. The behaviour of a single market can have macroeconomic consequences (a rise in domestic demand for cars affects an economy's trade balance, for example), and macroeconomic conditions shape the choices made within individual markets.

2.2Economics as a social science

Economics is a social science. The 'social' aspect comes from its subject matter — human behaviour, particularly the ways in which people seek to satisfy their needs and wants.

The 'science' aspect comes from how economists work. Like scientists in the natural sciences, economists propose theories about how the economy functions, then investigate those theories against observation. A simplified version of the process is shown in Figure 2.3: a problem is defined, a theory is put forward, the theory is investigated, and it is then either accepted or rejected. New theories are continually being developed to explain the rapidly changing global economy.

Theories in economics are usually called models. A model is a simplified representation of what actually happens, often expressed mathematically. The value of a model is that it can be applied repeatedly to test the same idea across many different contexts.

2.3Positive and normative statements

Economists can analyse facts without making any value judgement. Statements of that kind are called positive statements — they describe what is, has happened, or will happen, based on evidence or observation. Examples include 'a fall in the supply of petrol leads to an increase in its price', 'a 10% rise in tourist numbers has produced 10% more jobs in the tourism sector', or 'the inflation rate this year is 8%'. None of these statements contains the economist's own opinion.

When an economist includes an opinion or a value judgement in their analysis, the statement becomes a normative statement. A normative statement cannot be proven, because it claims something about what should, ought to, or might be the case rather than what is the case. The same factual situations above can be reworded normatively: 'a fall in the supply of petrol should lead to an increase in its price', 'a 10% rise in tourist numbers is likely to create at least 15% more jobs', 'the 8% inflation rate was the worst in ten years'. The italicised words signal the value-laden content.

A normative statement involves opinion or a value judgement that cannot be tested factually. Option B – calling negative externalities 'the most serious' market failure – ranks them subjectively. Options A, C and D describe testable cause-and-effect predictions (subsidies raising supply, higher incomes raising demand for normal goods, higher taxes weakening work incentives), all of which are positive.

2.4Meaning of the term ceteris paribus

Real economic situations are influenced by many variables at the same time. Economists use the Latin phrase ceteris paribus — meaning 'other things equal' — to simplify analysis. The phrase signals that, apart from one specified change, every other relevant variable is being held constant. The economist can then isolate and study the effect of that single change.

The most familiar use of the phrase is in the analysis of demand. When studying how a change in the price of a product affects the quantity consumers wish to buy, all other factors influencing demand — incomes, the price of substitutes, tastes, fashion, expectations — are assumed not to change. Only in that way can the resulting effect be attributed to price alone. The same logic applies throughout the syllabus: whenever you read or write an explanation that depends on one factor moving while others are held constant, the term ceteris paribus belongs in your answer.

The margin

Like ceteris paribus, the idea of the margin is a simplifying tool. Many problems in microeconomics are analysed in terms of marginal decisions — what happens when one variable changes by a small amount. A small rise in consumer income, for example, will produce small additional changes in consumer spending; some of that extra spending will fall on imports, so import volumes will also change a little. Examining the effect at the margin allows economists to predict the direction and approximate size of these changes.

Key concept link — the margin and decision-making

Decision-making by consumers, firms and governments is based on choices at the margin. For example, firms will produce up to the point where the revenue generated by an extra unit of output is equal to the cost of producing it. This concept - like scarcity and choice - can be applied in many different situations that economists study.

Ceteris paribus is a methodological device used to isolate the impact of one variable by assuming all other influences are held constant. Option B – 'everything else remains unchanged' – captures this. Option D is too narrow (it freezes the variable being studied), while A and C describe unrelated ideas (resource quality and rationing by price).

2.5The importance of time periods

Economic situations evolve over time, and economists distinguish carefully between what can be changed in the immediate future and what can be changed over longer horizons. Three time periods are used to model how factors of production behave under different constraints.

In the short run, a firm can change at least one factor of production but not all of them. The typical example is labour: the firm hires more (or fewer) workers while keeping capital, land, and enterprise unchanged. Ceteris paribus, hiring more labour can allow the firm to produce more — but only up to the limits imposed by the factors that remain fixed.

In the long run, all factors of production become variable. The firm can build a new factory, install more capital equipment, train its workforce, or move into new markets. Because the firm has time to plan, it can usually arrange its inputs more efficiently in the long run than it can in the short run.

In the very long run, all factors of production are variable and so are all other key inputs into production — including the state of technology, government regulations, and broader social conditions. The concept of 'Time' is often used to draw attention to whether the relevant distinction in a particular question is between the short run and the long run, or between the long run and the very long run.

These time periods do not correspond to a fixed calendar length such as three months or one year. The boundary between short run and long run is defined by which inputs can be varied, and that depends on the industry and the technology involved.

The long run is the planning horizon over which a firm can adjust every input. Option B – the time period when all factors of production are variable – matches this textbook definition. Option D describes the short run, while option C narrows the claim to 'key inputs' rather than all factors, and option A confuses variability with specialisation.

End-of-chapter practice

Past-paper questions from CIE 9708. Pick A, B, C or D. Answers are saved on this device — press Download report (PDF) at the top to save them.

In the long run, all factors of production are variable but the state of technology is fixed; in the very long run, technology itself can change. Option B – the ability to change the state of technology – is therefore the defining feature that separates the two horizons. Variable factors (D) already exist in the long run, so cannot be the distinguishing characteristic.

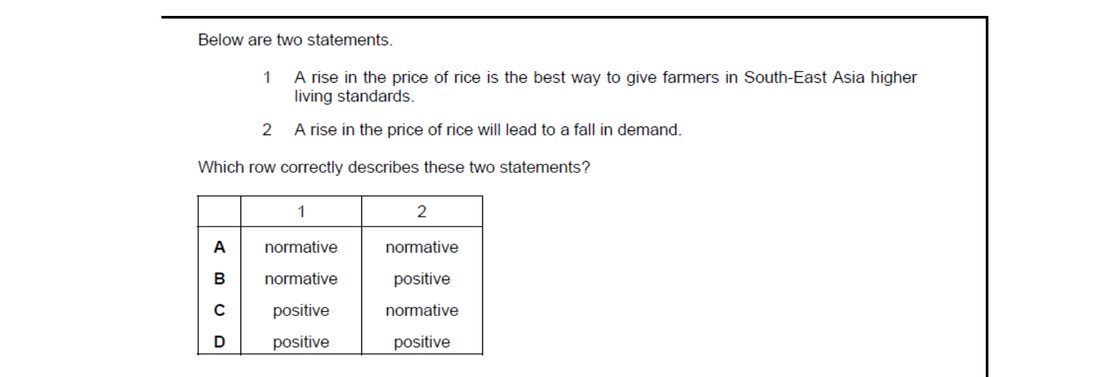

Statement 1 claims rising rice prices are the 'best' way to lift farmers' living standards — a value judgement, so normative. Statement 2 predicts that higher prices cause demand to fall, a testable cause-and-effect claim consistent with the law of demand, so positive. Option B – normative then positive – matches this pairing.

Positive economics deals with objective claims that can be verified or refuted using data. Option C states exactly this. Option B wrongly attributes objectivity to normative economics; option D wrongly makes positive economics subjective; option A confuses normative analysis with the description of models, which is positive in nature.

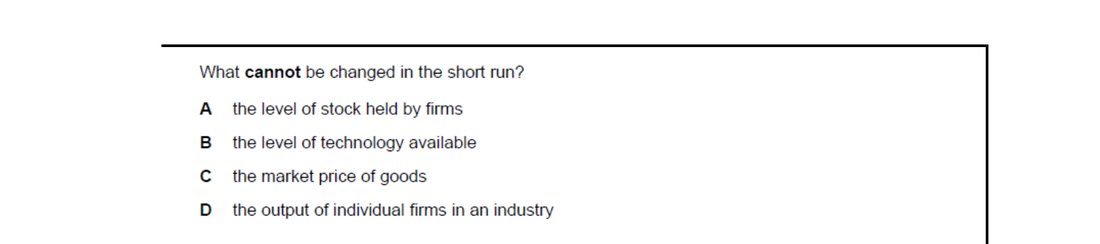

The short run is defined by at least one fixed factor; technology is treated as fixed in both short and long run and only changes in the very long run. Option B – the level of technology available – therefore cannot be altered in the short run. Stock levels, prices and individual firms' output (A, C, D) can all adjust quickly.

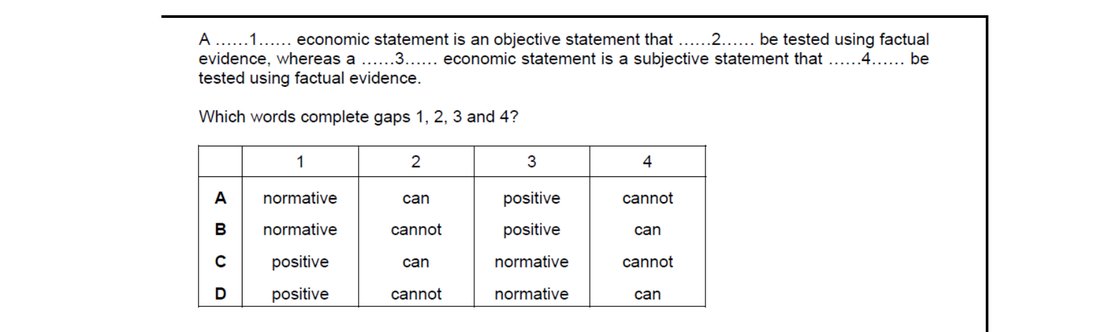

Positive statements are objective and testable against evidence; normative statements are subjective value judgements that cannot be settled by data alone. Option C correctly fills the gaps: gap 1 'positive', gap 2 'can' (be tested), gap 3 'normative', gap 4 'cannot' (be tested). The other rows scramble this positive/normative-versus-testable pairing.

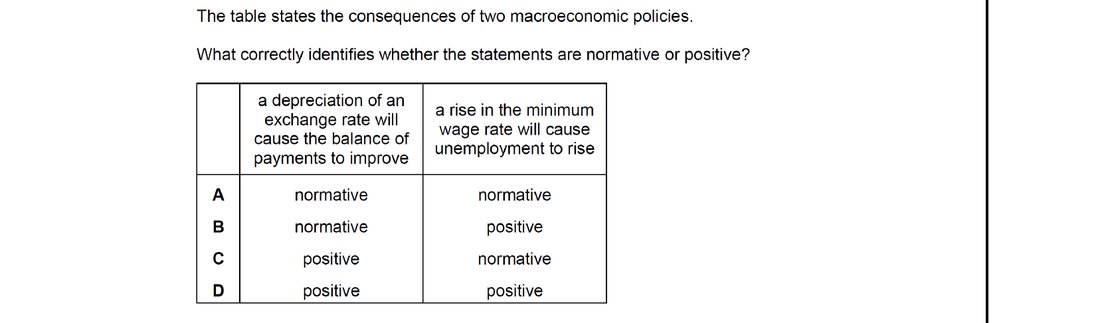

Positive statements are testable factual claims; normative ones contain value judgements. Statement 1 (taxes cause unemployment to rise) and statement 2 (the policy improves the balance of payments) are both cause-and-effect predictions about the economy that can be verified against evidence — neither uses 'should' or 'ought'. Option D – both positive – correctly classifies them.

Positive economics uses objective, evidence-based language. Option D – 'actual, ethics, fact, was, testable' – contains the most words tied to verification and factual description (actual, fact, was, testable). The other lists are dominated by value-laden terms ('should', 'better', 'ought', 'bias', 'opinion', 'moral'), which signal normative reasoning.

Attempt the practice questions above to build your score.

Self-evaluation checklist

After studying this chapter, you should be able to:

- Understand why economics is a social science.

- Understand the difference between positive statements and normative statements.

- Use the term ceteris paribus to describe a situation where 'other things remain equal' or unchanged.

- Understand the importance of time periods to assess how over time, change can influence the concepts that economists seek to model and explain.

Want more practice? Drill this chapter's past-paper MCQs (45 questions) →